Pricing DeFi Lending Risk: Repo, Puts, Tokenized Funds

There is a useful debate on CT happening around whether DeFi lending should be priced as a repo or as some form of short put exposure. Prime lending against liquid crypto collateral can behave a lot like overcollateralized repo. But once DeFi moves into looping structures, illiquid collateral, and especially tokenized funds, the assumptions that make the repo analogy appealing begin to fail. Prime crypto collateral, looping markets, and tokenized funds as collateral are three different financing regimes with three different failure modes.

Categorization

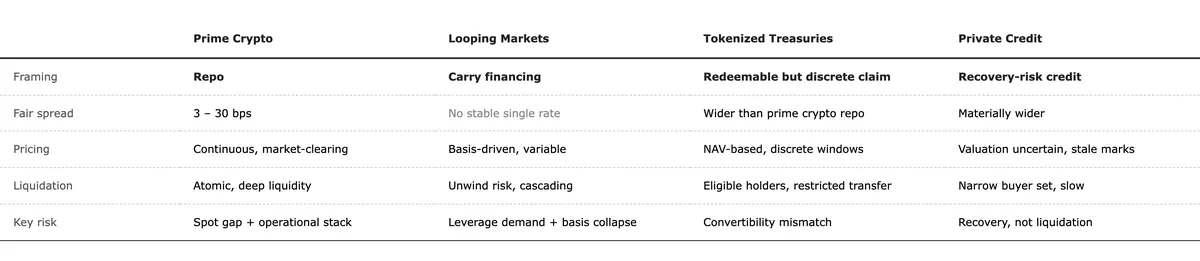

| Regime | Framing | Spread over risk-free |

|---|---|---|

| Prime crypto lending | Repo | 3–30 bps if calibrated to low observed lender bad debt |

| Prime crypto lending (tail-risk framing) | Short put / short convexity | 45 bps floor, then 130–350 bps, with 250–400 bps as Luca’s realistic band |

| Looping markets | Financing for carry trades | No stable single “fair spread”; driven by basis economics, leverage demand, and unwind risk |

| Tokenized treasury funds as collateral | Redeemable but discrete claim | Should price wider than prime crypto repo because convertibility is discrete, not atomic |

| Tokenized private credit funds as collateral | Recovery-risk credit | Should price materially wider again, because valuation, liquidation, and recovery are all slower and less certain |

The Debate

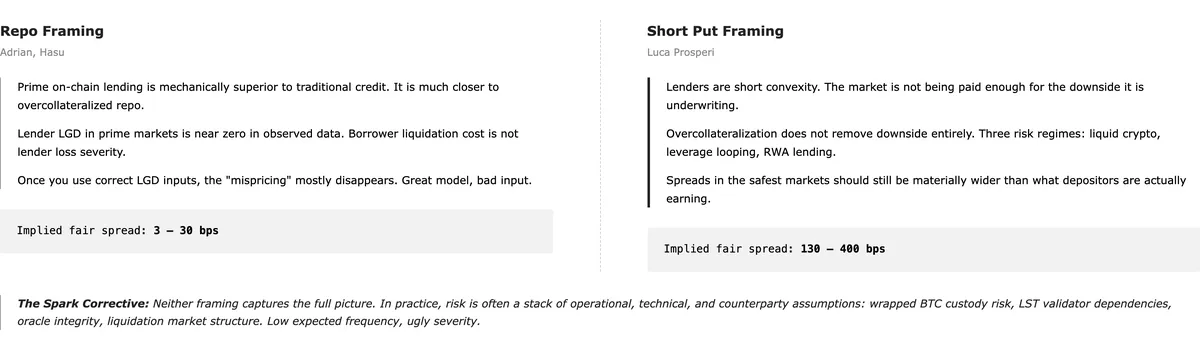

Luca Prosperi’s argument is the most rigorous version of a concern many people have felt for a while but rarely formalized properly. His claim is not simply that lending on Morpho is “risky.” It is that the market, particularly on the lender side, is not being paid enough for the downside it is underwriting. His framework breaks Morpho into three risk regimes: liquid crypto collateral, leverage looping, and RWA lending. In the first regime, he concedes that onchain lending is mechanically superior to traditional credit in important ways. In the third, he argues that most of the assumptions that make quant-friendly lending models work begin to fail at once: volatility becomes difficult to observe, marks go stale, liquidation is no longer truly atomic, and legal claims cease to be immediately enforceable. His conclusion is that spreads in the safest markets should still be materially wider than what depositors are actually earning.

Adrian’s rebuttal is narrower, but strong where it is narrow. His point is not that onchain lending is riskless. It is that the specific payoff being modeled in Luca’s framework is wrong for prime markets. In his telling, prime onchain lending is much closer to repo than to systematically selling puts. The key disagreement is around LGD. Luca’s setup effectively loads meaningful lender loss into the model; Adrian argues this confuses borrower liquidation cost with lender loss severity. If lender LGD is set closer to observed bad debt in prime markets, instead of something resembling the liquidation incentive, then fair spreads collapse toward the low single- to low double-digit basis points that are actually observed. In other words, the “mispricing” mostly disappears once the product is described correctly.

Hasu’s version of the same rebuttal is basically “great model, bad input.” This is useful because it makes explicit what the argument really is. Not whether tail risk exists, but whether the empirical assumptions being loaded into the model correspond to realized lender outcomes in the segment under discussion. If prime markets have historically generated very little bad debt for lenders, even through significant liquidations, then it is not enough to point to a stylized tail and declare the market irrational.

The Spark-side response adds the most important corrective. It shifts the debate away from clean market-risk stylization and toward the uglier category of fundamental risk. In practice, the problem in prime markets is often not simply that ETH might gap down too fast. It is that wrapped BTC has issuer and custody risk, LSTs have validator and smart contract dependencies, oracles have integrity risk, and liquidation systems depend on market structure that may only look deep until it isn’t. In other words, the risk is real, but it is not always best described as a neat option-like market exposure. It is often a stack of operational, technical and counterparty assumptions with low expected frequency and ugly severity.

Implications for Tokenized Funds as Collateral

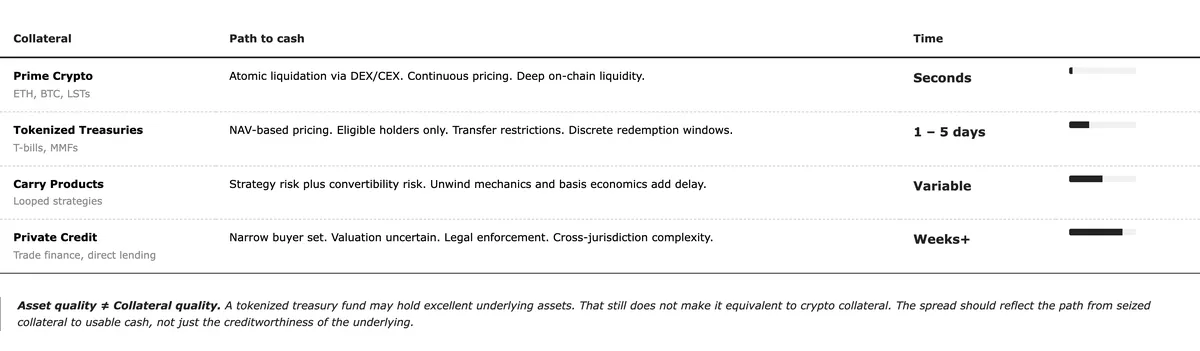

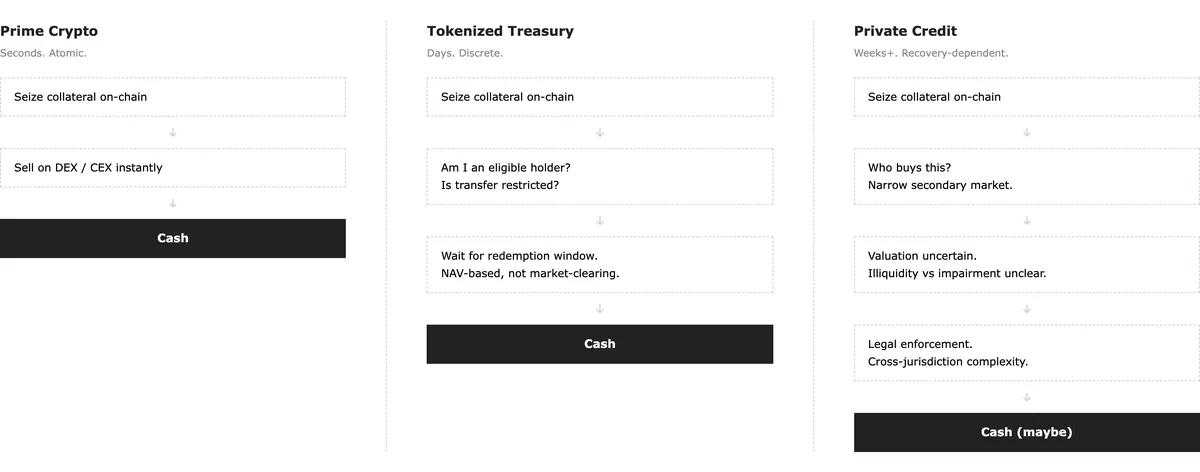

With tokenized funds, the key problem is not just volatility, or even just default in the usual sense. It is convertibility. More specifically, it is the mismatch between a funding structure that is continuous and a collateral base that is not.

If the collateral is a tokenized treasury fund, the underlying asset quality may be excellent. That still does not make it equivalent to crypto collateral. The question is not whether the fund is “safe.” The question is how quickly, by whom, and through what mechanism that position can be turned into cash in a liquidation scenario. If redemption is only available on certain windows, if transfer is restricted, if a liquidator needs to be an eligible holder, if the reference mark is NAV-based rather than continuously market-clearing, then the lender is financing something very different from prime crypto collateral even if the wrapper looks clean onchain.

That is where I think a lot of the discourse starts to lose relevance. The repo framing remains partly useful in the sense that one still cares about liquidation mechanics, haircuts, and realized lender loss. The short-put framing remains partly useful in the sense that tail events still matter and overcollateralization does not remove downside entirely. But neither really gets at the core issue for tokenized funds, which is that lender risk starts depending less on spot price moves and more on the path from seized collateral to usable cash.

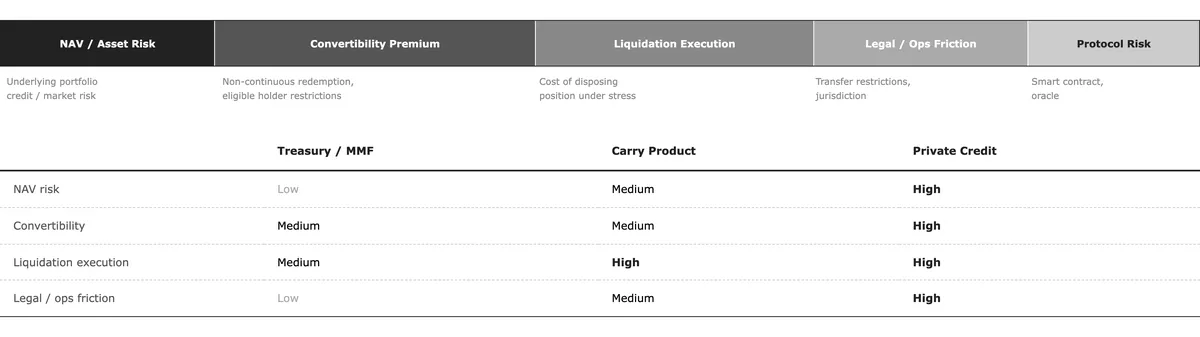

The spread over the risk-free rate should not be treated as one monolithic compensation for “risk.” It should be broken down into at least a few separate components. There is whatever underlying asset or NAV risk exists in the fund itself. Then there is a convertibility premium, which is compensation for the fact that the collateral may not be redeemable continuously or by everyone. Then there is a liquidation execution premium, which reflects the cost and uncertainty around actually disposing of the position under stress. Then there is legal and operational friction. And on top of that there is still the usual protocol, oracle, and smart contract risk that people are already familiar with from crypto lending more generally.

For something like a tokenized treasury or money-market fund, the first component may be small. The underlying portfolio is not the issue. But the convertibility and execution components are not zero, and I think that matters more than most people currently admit. Even in a relatively conservative case, it seems hard to argue that the required premium should collapse all the way down to prime crypto levels if the collateral cannot be realized with the same speed and certainty. The asset may be safer in one sense and worse collateral in another.

For carry products, the same logic applies but with a wider spread. Here the lender is not just financing a claim on low-risk assets. There is strategy risk in the underlying product, plus the same issues around convertibility and eligible buyer base. If the product only works economically because it can be financed at something close to prime crypto repo levels, then that itself is probably telling you the market is leaning too hard on the wrapper and not enough on the substance.

Private credit funds are where this becomes much harder to ignore. At that point the lender is no longer mainly relying on liquidation mechanics to protect principal. The lender is relying on recovery. Valuation becomes less certain, redemption becomes slower, the natural buyer set becomes narrower, and the distinction between temporary illiquidity and actual credit impairment becomes less clean. That does not mean the trade cannot work. But it does mean the premium required to finance that collateral should look materially wider, and in a lot of cases it may simply be too wide for the structure to remain interesting unless the underlying yield is high enough to absorb it.

My goal is to move toward a better quantitative framework for evaluating tokenized funds as collateral, anchored in the still limited but growing body of market activity around lending against tokenized assets. This feels like a central question if tokenized funds are meant to become a durable growth avenue for DeFi rather than a short-lived narrative: the structure has to offer real utility to both onchain lenders and borrowers, and the risk has to be legible enough to price.

Enjoyed this blog post? Consider subscribing: